Most people in a country don’t understand the intricacies of exchange rate management. Nevertheless, actions in this regard have significant implications for the economic stability, growth and overall success of the economy, on which human development is fostered.

This Insight explains how a professional approach to the management of the exchange rate seems to have been trumped by political considerations for much of 2015. The losses suffered by a lack of professionalism are not too different to the losses suffered due to corruption, and the lack of professionalism and corruption tend to be parasitic on each other. Therefore, this Insight also points to an important focus that has not yet been adopted by the agenda for good-governance.

What is an exchange rate, and why does it change?

The exchange rate between the Sri Lankan rupee (LKR) and the US dollar (USD) is the price of a USD in LKR, and like any other price, it is determined by demand and supply of USD in the country. The supply of USD comes from exports, worker remittances, tourist earnings, foreign investments as well as foreign loans, and other such inflows of foreign currency into the country. The demand for USD is created by imports, capital and interest payments for foreign loans, and other such foreign currency outflows from the country. When the demand for USD increases, given no change in supply, its value in LKR terms increases. This means that more LKR is needed to buy a USD, or in other words the value of the LKR has depreciated.

The role of the Central Bank

The Central Bank always maintains reserves of foreign currency (USD) to provide for the foreign currency payments needed for imports and other such outflows. These reserves can also be used to influence supply and demand for USD in the market, and thereby the exchange rate. For instance, the Central Bank can sell some of the reserves and by that increase supply. In doing so, it will reduce the price of USD and prop up the value of the LKR. If the reserves run low, the Central Bank will be forced to buy USD, and that will cause the LKR to depreciate. It is an expected function of the Central Bank to manage short term volatility by intervening in the market; this manages excessive daily volatility due to very short-term fluctuations of demand and supply in the market.

However, it is also possible to use these interventions irresponsibly to drive exchange rates to artificial values that cannot be sustained for too long. There is a pattern of such irresponsible action over several decades, which then resulted in sudden sharp periodic adjustments of the exchange rate that cause a shock to the market. This pattern was expected to change in 2015, but it didn’t.

Exchange rates held steady to serve political agendas

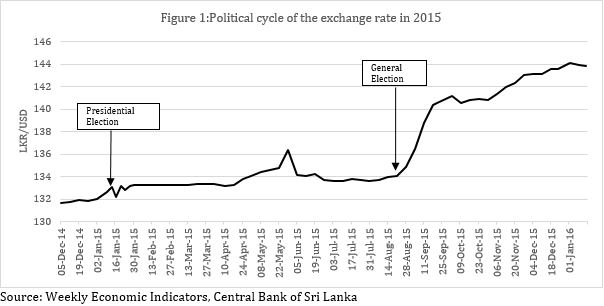

2015 was a year of two elections. The Presidential Election on January 8th, and the General Election on August 17th. In Sri Lanka, there is general public sentiment – reinforced through poor economic reporting in the media – that the value of the LKR is a sign of economic strength, and that a weak LKR corresponds to a weak economy. Depreciation of the currency also feeds back into inflation by increasing the LKR cost of imported goods, which are a significant part of consumption in Sri Lanka. This increases the political interest in the manipulation of the exchange rate close to elections.

Numbers show that between January to September 2015 the Central Bank acted to shore up the political interests of the incumbent government – by unsustainably shoring up the value of the LKR, rather than performing its professional duty of managing volatility and ensuring a stable rate of change in the exchange rate.

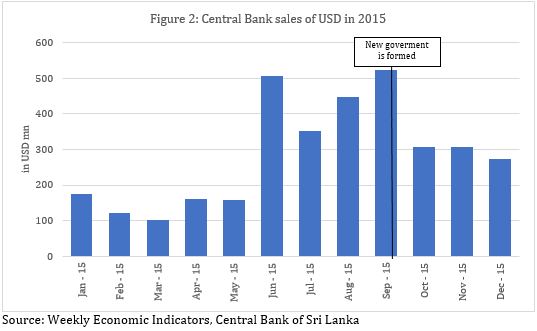

Figure 1 shows how the value of the USD shot up after the August election, in a shock adjustment, instead of finding a smooth path to its current value. Figure 2 shows how the Central Bank aggressively sold over USD 1.8 billion in the first eight months of 2015 in order to ensure an exchange rate that remained artificially high between LKR 133 and 134 up until the August General Elections was completed and government formed (which took another month after the election).

There are economic interests as well to distort exchange rates

There are economic interests mooted as well in maintaining an overvalued LKR. For instance, when USD loans become due and the government has to buy USDs to make the payment, the cost can be cushioned by an over-valued exchange rate. But the economic benefits are questionable when the rates cannot be maintained, because there is a significant loss suffered as well – by selling USDs at a lower price – to maintain the over-valued exchange rate.

Economics before politics

The manipulation of the exchange rate and the subsequent letting go highlights how the Central Bank has allowed political considerations to trump professional considerations in the management of the exchange rates.

This type of failure in professional management leads to huge invisible costs. It causes foreign investors to pause and assess much greater risk with regard to investments in Sri Lanka – thus driving up costs and reducing opportunities to attract investment. It causes losses and risks for all firms dealing in foreign trade, because unforeseen and sudden adjustments that arise from the unplanned impact.

If the economy was well governed and parliament was working with responsibility, the Central Bank should have been called upon to explain to the parliament and the public this apparent failure in professional management of the exchange rate.

It is not possible to wish away short term political interests, which are contrary to the long term interests of the country in the arena of policy making and governance. This provides a good reason for state institutions in a democracy to be

professionalised and insulated from undue political manipulation of their functions.

At present Sri Lanka has an agenda for fighting corruption, even if progress is slow. However, the present analysis shows that there is a need to expand the good-governance agenda to ensure that state institutions are held accountable to the public and parliament for the professionalism of their actions and performance.